Running a small or medium-sized business in Australia comes with a lot of moving parts. Between managing staff, serving customers, and keeping cash flow steady, tax planning is one of those things that often gets pushed to the side until the end of the financial year. But that approach costs business owners real money every single year.

In 2026, the tax landscape for Australian SMEs has shifted in some important ways. The ATO has tightened its focus on compliance, new thresholds have been updated, and there are fresh opportunities that smart business owners are already taking advantage of. Whether you are a sole trader, a company, or a trust, the strategies below are designed to help you keep more of what you earn.

Why Tax Planning Matters More Than Ever for SMEs

Tax planning is not about dodging obligations. It is about understanding what the law allows and making deliberate decisions before the financial year ends. The difference between a business that plans and one that does not can easily be tens of thousands of dollars.

For SMEs operating in Australia, the Australian Taxation Office provides a clear framework for what deductions, concessions, and structures are available. The problem is that most small business owners are either not aware of all their options or do not have the time to action them properly.

This is where a structured approach to tax planning strategies Australia-wide becomes essential, not just a nice-to-have.

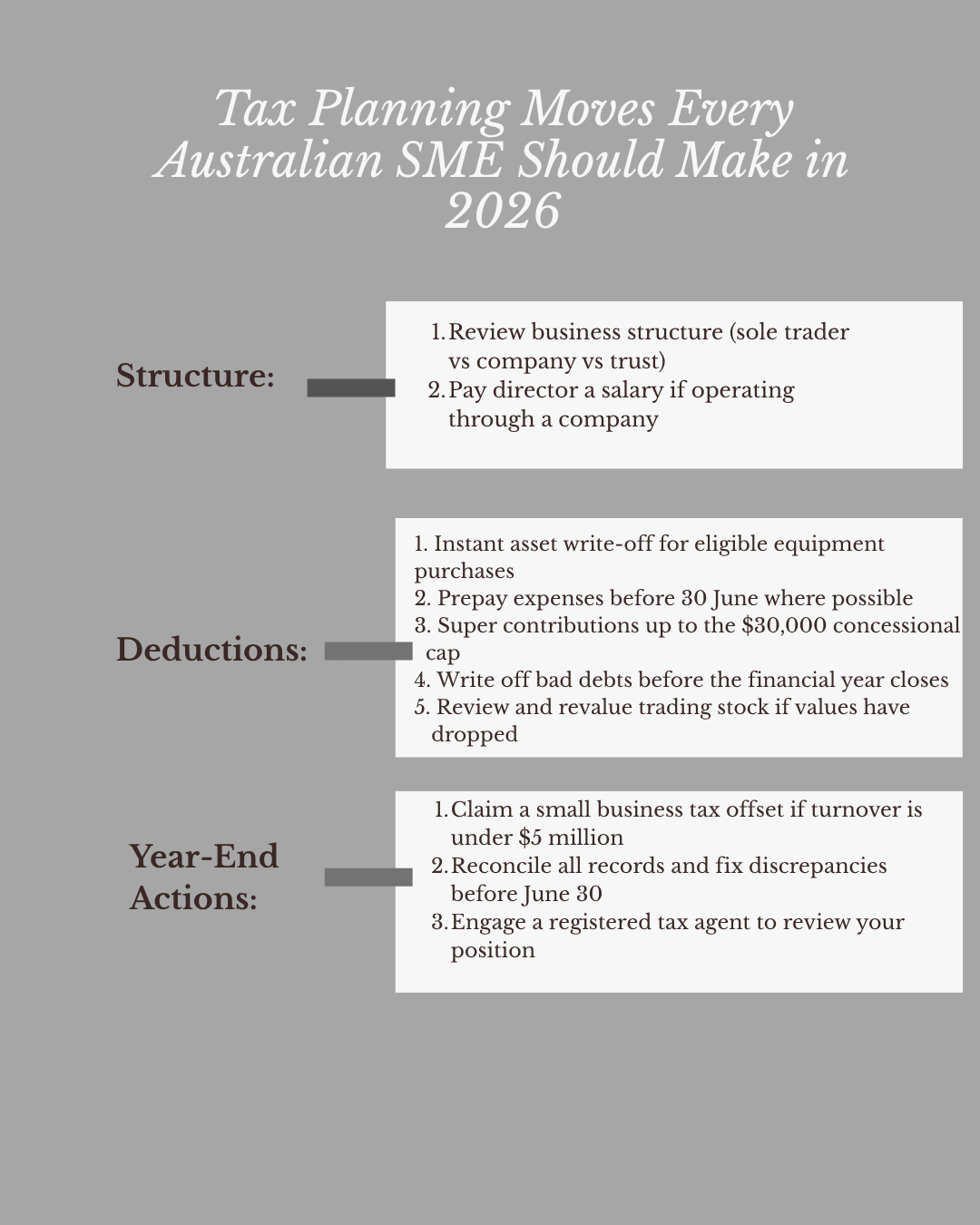

1. Get Your Business Structure Right

One of the most impactful decisions you will make is the structure through which your business operates. Sole traders, partnerships, trusts, and companies all carry different tax implications, and what suited you five years ago may no longer be the most efficient option today.

Sole traders pay tax at individual rates, which can climb steeply as income rises.

Companies are taxed at a flat rate of 25 per cent for base rate entities with turnover under $50 million, which can be significantly lower than the top marginal rate.

Discretionary trusts allow income to be distributed to beneficiaries in lower tax brackets, potentially reducing the overall tax burden for family businesses.

If your current structure is no longer the right fit, the start of the financial year is the best time to consider restructuring. The ATO provides small business restructure rollover relief that can help you make the transition without triggering a capital gains tax event in many cases.

2. Make the Most of the Small Business Tax Offset

If you are a sole trader or receive a share of net small business income, the small business tax offset could reduce your tax by up to $1,000 per year. It applies if your aggregated turnover is less than $5 million.

This one is surprisingly underused. Many business owners are eligible but either forget to claim it or assume their accountant is handling it. It is worth confirming each year that this offset is being applied to your return.

3. Instant Asset Write-Off: Still One of the Best Concessions Available

The instant asset write-off has been one of the most discussed measures for Australian SMEs over the past few years. As of the 2025-26 financial year, eligible businesses can immediately deduct the cost of assets used in their business, subject to the applicable threshold at the time of purchase.

Practically speaking, this means that if you buy equipment, tools, technology, or machinery for your business before the threshold period ends, you can deduct the full cost in the same year rather than depreciating it over several years. This brings your taxable income down now rather than gradually.

Check the current threshold with your tax agent, as this has changed more than once in recent years, and the amount that applies depends on when the asset was first used or installed ready for use.

4. Prepay Expenses Before 30 June

One straightforward and perfectly legal strategy is prepaying eligible business expenses before the end of the financial year. If you prepay expenses that cover a period of 12 months or less and the period ends before 30 June of the following year, you can generally claim the deduction in the year of payment.

Common examples include:

- Business insurance premiums

- Rent for business premises

- Subscriptions and software licences

- Professional memberships and training

- Interest on business loans

This works particularly well in a year where your income is higher than expected, and you want to bring some deductions forward.

5. Superannuation Contributions as a Tax Tool

Superannuation is one of the most tax-effective environments available to Australian business owners. If you are a sole trader or a company director, making personal concessional contributions to your super fund can significantly reduce your taxable income.

For the 2025-26 financial year, the concessional contributions cap sits at $30,000 per person. Contributions made within this cap are taxed at just 15 per cent inside the fund rather than at your marginal tax rate, which for many SME owners could be 32.5 per cent or higher.

The catch-up concessional contributions rule also allows individuals with a total super balance below $500,000 to carry forward unused cap amounts from up to five previous years. This can be a powerful option if your income has jumped sharply this year.

According to Money Smart by ASIC, making voluntary super contributions is one of the most overlooked retirement and tax planning strategies available to self-employed Australians.

6. Write Off Bad Debts Before Year-End

If your business uses accruals accounting, you may have invoices that were issued but are unlikely to ever be paid. These bad debts can be written off as a deduction, but only if you take formal steps to recognise them as bad before 30 June.

This means reviewing your debtors list, making a genuine decision that specific amounts are not recoverable, and documenting that decision in writing before the financial year closes. Simply hoping the payment will arrive eventually does not qualify.

7. Review Your Trading Stock

For businesses that hold trading stock, there is a choice each year about how to value that stock. You can use the cost price, the market selling value, or the replacement value. If your stock has decreased in value due to damage, obsolescence, or falling market prices, switching to a lower valuation method can reduce your taxable income for the year.

This is a simple adjustment, but one that many business owners overlook entirely, particularly when they are not being actively guided through a year-end checklist by their accountant.

8. Pay Yourself a Salary from Your Company

If your business operates through a company and you are a director, paying yourself a salary instead of drawing dividends can be more tax-efficient depending on your circumstances. A salary is a deductible expense for the company, which lowers its taxable profit. Your personal income will be subject to individual rates, but you will also become entitled to the tax-free threshold, low-income tax offset, and other individual concessions.

This requires proper setup through your payroll system and must be reported correctly. Getting advice from a registered tax agent before making changes here is strongly recommended.

9. Keep Your Records Immaculate Year-Round

One of the most effective tax planning strategies Australia has to offer is also the least glamorous. Clean, accurate, up-to-date record keeping throughout the year means you are never scrambling at tax time, never missing deductions, and never exposed to penalties for poor documentation.

The ATO has become increasingly data-driven, matching information from banks, share registries, employers, and payment systems. If your records do not reconcile with what the ATO already knows, you are likely to receive a review or audit notice.

Using cloud-based accounting software that integrates with your bank feeds is the minimum standard most businesses should be operating at in 2026.

10. Engage a Registered Tax Agent Who Understands Your Industry

Generic tax advice can only take you so far. A tax agent who understands the specific deductions, structures, and concessions relevant to your industry will almost always save you more than their fee costs. Whether you are in hospitality, construction, retail, professional services, or health care, the nuances matter.

If you are based in the Illawarra region, getting local advice from specialists who understand both national tax law and regional business conditions makes a real difference. The team at Wollongong Taxation Services helps SMEs across the region build practical, compliant tax strategies that work year after year.

Tax Planning Snapshot for Australian SMEs 2026

Ready to Stop Overpaying Tax? Let Us Help

Most SMEs in Australia leave money on the table simply because they do not have the right advice at the right time. The strategies above are a strong starting point, but the real savings come from applying them to your specific numbers, industry, and business structure.

At Wollongong Taxation Services, we work with small and medium business owners across the Illawarra and beyond to build tax strategies that are practical, compliant, and genuinely impactful. Whether you want a one-off review before 30 June or ongoing advisory support throughout the year, we are here to help.

Book your free 20-minute tax planning call today. No jargon, no pressure. Just a straight conversation about where your business stands and what you could be doing better.

Frequently Asked Questions

What are the best tax planning strategies for small businesses in Australia?

The most effective strategies include reviewing your business structure, maximising superannuation contributions within the concessional cap, claiming the instant asset write-off, prepaying eligible expenses before 30 June, and writing off bad debts. The right combination depends on your specific turnover, structure, and industry.

When should I start tax planning for my business?

Ideally, tax planning is something you revisit throughout the year rather than leaving it to the last few weeks of June. Starting a structured review at least three months before 30 June gives you time to action the most valuable strategies, particularly those involving purchases, contributions, or structural changes.

Can I change my business structure to reduce tax?

Yes, in many cases, you can restructure your business through the ATO’s small business restructure rollover provisions without triggering an immediate tax liability. However, restructuring has legal and compliance implications beyond tax, so it should always be done with proper professional advice.

Is the instant asset write-off still available in 2026?

As of the 2025-26 financial year, eligible small businesses can still access immediate deductions for certain asset purchases. The specific threshold and eligibility criteria should be confirmed with a registered tax agent, as these have been subject to legislative changes in recent budget cycles.

How much can I contribute to my super to reduce my tax?

The concessional contributions cap for the 2025-26 financial year is $30,000 per person. Contributions within this cap are taxed at 15 per cent inside the fund. If you have unused cap amounts from previous years and a super balance below $500,000, you may be able to contribute more under the carry-forward provisions.

What records do I need to keep for tax purposes?

The ATO requires most business records to be kept for at least five years. This includes income records, expense receipts, bank statements, payroll records, depreciation schedules, and any documents supporting deductions you have claimed. Digital copies are accepted provided they are clear and accessible.